Uncategorized

You want a subscription to <!–Startup Investor–> to view this content material.

The put up Startup Deal Stream Altering appeared first on Early Investing.

0

You want a subscription to <!–Startup Investor–> to view this content material.

The put up Startup Deal Stream Altering appeared first on Early Investing.

Within the wake of the bulletins of Fb’s Libra and the Chinese language authorities’s intention to have a Central Financial institution Digital Foreign money (CBDC), the subject of CBDCs as a brand new element of a rustic’s authorized tender has change into well-liked with governments and commentators. The essential thought is to have fiat cash represented in digital type. Whereas most, if not all fiat currencies presently have a digital type (central banks create and monitor their currencies on computer systems), the CBDCs beneath dialogue would result in multi-functional digital cash that is ready to transfer within the digital world (from laptop to laptop and different units) quite than simply sit static on a database. It could even be programmable such that its actions could possibly be automated. Many theorize about how such a fiat digital forex would revolutionize cost techniques and different digital monetary and business actions via effectivity, comfort, and flexibility.

the #CBDCs beneath dialogue would result in multi-functional digital cash that is ready to transfer within the digital world

How this new digital cash would work from a coverage, financial, and architectural standpoint additionally has spawned a lot dialogue. Sensible questions abound, similar to how a transition to digital cash may work, to what extent would fiat forex be solely digital in nature, what expertise would underly any such CBDC (e.g., blockchain or different distributed ledger versus a extra centralized database), who would maintain accounts on the central financial institution (e.g., solely the biggest banking establishments on a spectrum to each individual). Some have argued {that a} CBDC would clean the distribution of presidency support on this time of COVID-19. For a way of most of the key factors which have emerged within the dialogue of CBDCs, this text features a collection of hyperlinks to assets on the finish.

The aim of this text is to not catalog nor opine on the various concerns that numerous session papers, research, and articles do a very good job of figuring out and discussing if not really fixing. Examples of essential points which have come into account embrace private privateness,¹ the technical structure of a CBDC system,² and the potential macro impacts on the monetary system, in addition to financial and monetary coverage.³

Slightly, this text focuses on three explicit concerns which have acquired comparatively little consideration and makes an attempt to offer temporary however helpful ideas on every.

The primary is transparency, although not as the alternative of particular person privateness rights however across the structure and construction of all the CBDC system from each a technical and organizational perspective. Two questions summarize this subject: how is the expertise architected and programmed? Who performs what roles within the implementation?

The second little-noticed space issues interoperability. A CBDC could also be designed to have broad makes use of however the methods it may be used on or with different techniques is essential. This contains whether or not it may be traded or used as cost on digital asset exchanges and digital marketplaces for items and companies and whether or not it may be withdrawn and used like money. With out the power for a digital fiat forex for use extensively in commerce, the central financial institution is caught within the current, not making ready for the long run.

With out the power for a digital fiat forex for use extensively in commerce, the central financial institution is caught within the current, not making ready for the long run

Third, extra thought ought to be given to the systemic threat concerns of a digital fiat forex. I argue that CBDCs will, the truth is, lower systemic threat for most of the causes that robust fiat currencies create a stage of monetary stability but in addition as a result of it will carry a brand new range to the monetary system. After all, it’s incumbent on central banks to handle the forex nicely to ensure that systemic threat to stay in examine.

This text discusses every of those three concerns in flip.

CBDCs may show an important monetary innovation for the reason that finish of the Bretton Woods system. Personally, I’m a believer that governments ought to start to undertake CBDCs and assume that personal, fiat-linked digital “stablecoins” are the laboratories pointing the best way. These experiments are ripe for encouragement and research to assist chart the course for the profitable way forward for CBDCs.

Transparency could be a nuanced time period as a result of it’s usually utilized selectively. Individuals and organizations make selections about how a lot transparency they may allow: what to reveal what to maintain secret and from whom. In a radically clear situation, the whole lot is disclosed or at the very least seen on demand by everybody. Such an structure doesn’t respect privateness, which many CBDC commentators rightly describe as a elementary human proper. On the different finish of the spectrum is full privateness, the place no data is obtainable to anybody aside from the individual concerned.

This text isn’t targeted on questions of non-public privateness round transaction, identification or different data however quite on the transparency of the system itself and advocates for disclosure of the features, options and first actions round any CBDC, together with the rights and obligations of individuals. This transparency of the general design and structure would create the belief wanted for broad adoption of a CBDC. There are two major areas the place transparency ought to be necessary with the intention to set up integrity: the code on which the CBDC features, and the duties and liabilities of key actors.

With respect to the latter, a CBDC system ought to disclose the totally different individuals and their roles within the CBDC implementation, from the central financial institution and the direct account holders to the custodians of accounts, cost processors, pockets suppliers and different permissible intermediaries. The CBDC system ought to be clear in regards to the totally different actions and capabilities of every participant within the system.

The place does the digital cash come from and who creates it? Is the system account-based (balances are mirrored solely in consumer accounts) or token-based (digital gadgets are held straight by customers)? How are balances up to date and people updates verified?

What permissions does every participant have and do they differ in ways in which make sense given the position? Can they get well my account if I lose entry, repair errors, or make different adjustments? What kinds of accountability are constructed into the system and who’s answerable for them? What legal responsibility is related to every participant and their actions and the way is legal responsibility established such that they’re accountable? What compensation do they earn for his or her actions and the way is it set? How will the programmability of the forex, if any, work?

These are essential questions for the design and structure of the CBDC platform and must be recognized to all with the intention to create an acceptable stage of integrity and verification within the system. The Bitcoin blockchain establishes belief via reliance on open-source laptop code and the position of miners every checking the others’ work earlier than an replace can happen. These options maximize transparency to create belief, however they don’t seem to be the one option to create a Byzantine fault-tolerant platform (as a proxy for belief). Intermediaries will be trusted too however provided that their roles, duties, compensation and legal responsibility are well-understood. The alternatives of the CBDC designer with respect to actors on the platform might want to create Byzantine fault tolerance or different belief for all stakeholders.

The above issues participant transparency however there are additionally essential transparency points related straight with the programming of the software program. It should be an interactive, iterative course of that depends on crowdsourced expertise and competencies. Open supply code permits all stakeholders an equal potential to entry, learn and assess the pc code, search for bugs and bigger flaws, and in any other case check that the code features as disclosed and isn’t topic to exploits that can lead to hacks, stealing and even bringing the system down. A CBDC will want an equal means to let stakeholders belief the code and thereby belief the forex.

There might be objections to this stage of transparency, a few of them strongly said round nationwide safety and security. These complaints is not going to face up to scrutiny. Stakeholders are uninterested in secrecy about cash and the complicated techniques that create, distribute, and course of it. Individuals want readability across the workings of essential monetary processes of their lives to allow them to take part successfully, plan successfully, and be accountable customers. The huge preponderance of these stakeholders might be good individuals. Programs ought to be designed with transparency to encourage the great as a result of that marginalizes the unhealthy and leads to a platform extra more likely to notice its optimistic attributes and change into ubiquitous.

Furthermore, a lot of monetary companies regulation focuses on disclosure and transparency by regulated entities and their actions, techniques, processes and different trivia. These disclosure obligations stem from the best of creating it harder for unhealthy actors to thrive. There is no such thing as a good cause to exempt a CBDC from these ideas.

We see the identical traits past monetary companies. Within the COVID-19 disaster, extra transparency and data was used to “flatten the curve”, defend populations and their return from self- quarantine and rework manufacturing and provide chains to get wanted medical and different supplies to the locations that wanted them most.

Lastly, transparency creates resiliency, not solely from the standpoint of techniques that climate assaults but in addition techniques that evolve and improve to fulfill threats and challenges or simply make sensible adjustments that profit customers. Transparency will assist drive innovation each with respect to the CBDC platform and versatile utilization of the CBDC.

Nations that undertake CBDCs will need excellence as they exchange present techniques. Transparency will assist guarantee excellence; certainly, it’s a key function of excellence.

Nations that undertake #CBDCs will need excellence as they exchange present techniques. Transparency will assist to make sure excellence. Certainly, it’s a key function of excellence.

For a CBDC, interoperability is about its potential to be multi-functional and multi-platform, to play nicely with others. Excited about bodily money illuminates the idea.

Somebody carrying US {dollars} in money strolling round New York Metropolis should buy numerous issues. That’s a stage of interoperability. However that very same individual carrying US {dollars} in Paris has a lot much less potential to purchase. And that very same individual attempting to make use of bodily money on the web has misplaced all potential to spend it. Bodily money has pretty good interoperability within the bodily world when you’re in the precise nation however its interoperability declines rapidly outdoors its major context.

Digital cash, alternatively, can have glorious interoperability. Bank cards present the best way. The identical New Yorker carrying a bank card can spend cash in New York Metropolis, in Paris (as a result of the bank card firm and banks convert to the suitable fiat forex) and on-line as a result of the cost rails transfer the digital cash to the precise place (at the very least more often than not).

A CDBC may break down these limitations even additional. This concept is a part of the unique conception of Bitcoin: you possibly can spend it wherever just by utilizing your personal key to signal a switch out of your account to the recipient’s account. There is no such thing as a technological cause that prohibits a CBDC from fulfilling this promise. In reality, it is without doubt one of the major advantages of digital fiat cash. 5

Most #CBDC proposals usually are not contemplating interoperability as a result of they’re attempting to merely duplicate the present system. Such restricted imaginative and prescient will stifle the efficiencies and innovation that an interoperable CBDC can ship

Most CBDC proposals usually are not contemplating interoperability as a result of they’re attempting to merely duplicate the present system. Such restricted imaginative and prescient will stifle the efficiencies and innovation that an interoperable CBDC can ship. Put one other means, a CBDC designed to perform on or at the side of any platform will change into a reserve forex and dominate, or at the very least have a major position in, commerce for the following a number of generations. Everybody will need it as a result of it really works most in all places, making a easy retailer of worth and facilitating quick, environment friendly and fast funds. And including programmability to interoperable digital cash will additional develop the probabilities. Fiat-linked stablecoins, mentioned under, attempt to fill the present lack of interoperable digital cash, so the demand is obvious.

The kind of transparency mentioned above serves the reason for a really interoperable CBDC as a result of it permits all individuals and stakeholders to belief the digital cash and belief that it’ll perform in all or almost all contexts. CBDC has the good thing about being backed by the total religion and credit score of the federal government. Combining that backing with transparency and interoperability will lead to even greater ranges of belief within the CBDC and leads into our subsequent level.

Systemic threat is the concept monetary system collapse may happen on account of tight linkages between and amongst sure components, merchandise and/or actions when a number of triggering occasions occurs. The idea rose to prominence after the 2008 monetary disaster and there’s in depth literature on the subject, significantly from international monetary regulators. The assets on the finish of this text hyperlink to some gadgets for reference.

There are two major unknowns related to systemic threat:

(1) what’s going to set off it and

(2) why will the triggering occasion trigger monetary system collapse quite than simply remaining remoted to a single entity, sector, or nation.

Due to these unknowns, the regulatory response to systemic threat has been sweeping necessities designed to strengthen all establishments, unfold threat broadly amongst monetary markets individuals and conduct situation evaluation of various doable inside and exogenous “shock” occasions to research the circulate and unfold of doable repercussions throughout establishments, segments of the monetary markets and the worldwide monetary system as a complete.

A CBDC is only a new format for the fiat forex, so in that sense it shouldn’t introduce any new systemic threat. It might change a number of the plumbing of the monetary system in ways in which scale back operational and credit score threat however it isn’t a brand new instrument, it doesn’t change the denomination of something and it may be used precisely the identical as present cash (as a result of it actually is similar as present cash!).

A #CBDC is only a new format for the fiat forex, so in that sense it shouldn’t introduce any new systemic threat

However there are different forces at play, specifically fiat-linked stablecoins and the rise of digital ecosystems, each of which drive the continued drawing collectively of worldwide exercise, communications, information-sharing, commerce and markets. These tight linkages, along with present monetary devices and their markets, make it essential for CBDC creators to think about how CBDCs may also help decrease systemic threat by including belief and variety into the system.

For our functions, stablecoins are digital currencies designed to have a steady worth towards a fiat forex.6 They’re privately created and operated, generally on a decentralized foundation, and search to offer a technological bridge between blockchain belongings and fiat currencies. They make fiat currencies blockchain-friendly in order that transactions in fiat can happen on blockchains. Assessments of their doable dangers, systemic and in any other case, have been written, a collection of that are linked to under.

Digital ecosystems, which I generally seek advice from as “platforms as cities”, are merely self-organizing communities within the digital world. They’re generally centrally operated, like many social media platforms or multi-player on-line video games, but in addition will be decentralized, like public blockchains. These ecosystems will be business in nature but in addition can have many different functions, from easy communications to tutorial pursuits to gaming to political organizing to illegal exercise. The secret is that they appeal to individuals from across the globe and permit them to work together beneath a typical structure and algorithm.

Stablecoins and digital ecosystems are vital contributors to, and accelerators of, international closeness that may quickly permit anybody, wherever, to speak and commerce with anybody else wherever else, as long as they each have entry to a pc and the web. CBDCs will play an essential position within the monetary system because it grows to accommodate and serve digital ecosystems and international closeness. They’ll contribute to monetary stability throughout the digital realm and its ecosystems however provided that they respect the values of transparency and interoperability mentioned above.

The recipe may appear deceptively easy: govern responsibly so your forex is steady and ensure the CBDC can perform throughout platforms such that it coexists with all digital belongings, each conventional and newer. However it should additionally require the belief that comes with transparency and the interoperability that permits for range of choices, together with personal cash (like multi-purpose cryptocurrencies and fiat-linked stablecoins).

The second half, a number of kinds of cash, is likely to be simpler to conceptualize and combine as a result of we already dwell in a world of award factors, in-game gold, and pay as you go playing cards, to call a couple of present choices. Transparency, nevertheless, shouldn’t be too tough both, as we’ve got seen the rise of information assortment and availability coincide with disclosure-based regulation.

CBDCs supply at the very least two technique of decreasing systemic threat. First, fiat currencies already underpin almost all the monetary system, however the introduction of cryptocurrencies and decentralized finance. Second, fiat currencies profit from authorities backing, creating larger stability, significantly for developed economic system currencies.

Governments, central banks, and international establishments tout the advantages of fiat currencies. With the precise transparency and interoperability, the CBDC variations of fiat currencies may carry these advantages to the digital world.

The close to way forward for CBDCs among the many G-20 will contain a lot debate and lots of proposals. Stakeholders and commentators ought to decide the proposals throughout a variety of things however ought to be constant in advocating strongly in favor of proposals that skew in direction of transparency and interoperability that thoughtfully tackle systemic threat as a result of the three ideas are tightly coupled. Reimagining commerce and finance round a CBDC is enjoyable with the infinite prospects it permits. The results of the improper last design and implementation, nevertheless, will create new issues and exacerbate present situations. We should always do higher than that.

Governments, central banks, and international establishments tout the advantages of fiat currencies. With the precise transparency and interoperability, the #CBDC variations of fiat currencies may carry these advantages to the digital world

Lee A. Schneider is Common Counsel at Block.one, one of many world’s largest blockchain corporations and creator of the EOSIO blockchain protocol. In that position, Schneider is answerable for numerous points of the authorized perform in addition to the corporate’s authorities affairs initiatives. He joined Block.one after main the blockchain, Fintech, and broker-dealer practices at two main worldwide corporations. Lee has been acknowledged as one of many main voices in blockchain-related regulation and compliance and has performed a job in structuring a number of of the biggest and most profitable blockchain-related initiatives. Schneider co-hosts the Urge for food for Disruption podcast with Troy Paredes and is the contributing editor for the Chambers and Companions Fintech Observe Information. He’s the contributing editor of the Chambers and Companions 2019 Fintech Observe Information.

Chosen Sources-CBDCs:

Within the social media trade, an organization both innovates and grows — or it shortly dies.

In reality, firms within the trade are clear about this of their SEC filings.

Take Snap Inc. (SNAP) for example. In its IPO submitting, the corporate indicated that its progress, and its very survival, rely on its capacity to innovate.

Just lately, shares of Snap have rallied 116%. So it should have found out its innovation plan… proper?

Unsuitable.

No Patent Safety!

Lengthy earlier than Snap went public in March 2017, I used media appearances and print articles to warn traders to not contact it.

The rationale? It had no patent safety!

That’s why giants like Fb may copy Snap’s hottest improvements with impunity.

And Fb did copy Snap’s improvements:

It copied its “Lens” filters… its “Tales” format… its 3D face filters…. And so forth.

And for Snap, this was very unhealthy information…

It’s All In regards to the Community

You see, to make cash as a social media firm, you want an enormous userbase…

You want an enormous community you possibly can promote promoting to.

However with Fb “borrowing” all of Snap’s improvements, Snap’s community wasn’t rising quick sufficient.

And that’s why its losses began piling up.

In reality, within the quarter earlier than its IPO, its losses ballooned by 37%.

Look Out Beneath!

Once we put money into IPOs, we’re investing in an organization’s future progress and earnings.

So when the one factor an organization does is burn cash, look out under…

The inventory is doomed!

And positive sufficient, that’s exactly what occurred with Snap:

Earlier than lengthy, the inventory was down over 80% from its IPO-day excessive.

The Menace to the Present Rally

However traders have brief recollections…

That helps clarify why, based mostly on some new improvements (not patented), Snap’s inventory just lately rallied again to its $17 IPO worth.

This is unnecessary…

You see, along with competing with Fb, Snap is now competing with TikTok.

This China-based app for making and sharing brief movies already boasts an even bigger userbase than Snap worldwide…

And within the U.S., which is Snap’s largest market, TikTok is quickly gaining floor. In reality, within the final yr, its month-to-month lively customers almost doubled.

Moreover, TikTok has began “borrowing” Snap’s hottest options, identical to Fb does…

Copying a Cash Maker

In accordance with Digiday, a commerce journal for on-line media, TikTok is ready to launch a brand new advert format.

This format will let customers create movies utilizing “Augmented Actuality” results which are branded.

This can be a direct copy of Snap’s wildly profitable “Sponsored Lens” advert format.

And for TikTok and its advertisers, this guarantees to be an enormous success…

As Enterprise Insider’s Nina Goetzen and Daniel Carnahan defined just lately, TikTok’s options permit content material to go viral in a manner that simply isn’t attainable on Snapchat…

On Snapchat, content material solely will get unfold to a person’s instant circle. However TikTok’s “discoverability” options (like hashtags and its “For You” web page) make it attainable for content material to unfold infinitely.

Something Snap Can Do, Fb and TikTok Can Do Higher

Backside line:

Something Snap can do, Fb and TikTok can do higher.

And since there’s no patent safety to stop this competitors, Snap is doomed.

So don’t even assume about shopping for into the present momentum in Snap shares. It gained’t final.

As a substitute, be looking out for the IPO of TikTok’s mother or father firm, ByteDance.

That’s anticipated someday this yr.

Forward of the tape,

Lou Basenese

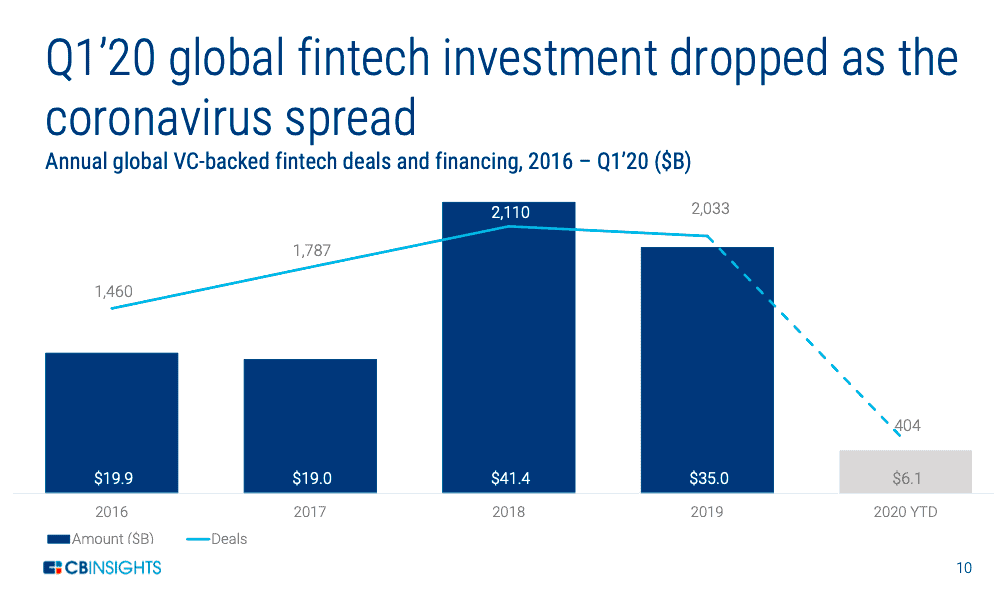

This could come as no shock however Q1 was horrible for VC-backed Fintechs because the Coronavirus pounded non-public capital markets and crash-landed the as soon as strong market. In accordance to CBInsights, the primary quarter of 2020 was one of many worst quarters for Fintech funding in years. Buyers pulled again (whereas nonetheless claiming they have been open for enterprise), mega-rounds stalled globally, and China reported simply 129 offers, elevating $175 million, through the quarter – the worst reported since 2015. Seed and angel rounds dropped to five quarter low.

Based on the report, complete Fintech funding totaled $6.079 billion throughout Q1 versus the identical quarter yr prior of $7.14 billion. Throughout This autumn of 2019, Fintechs raised $9.577 billion. The full variety of offers funded dropped to 2016 ranges with 404 accomplished transactions. Each area besides Africa noticed a decline in Fintech offers through the quarter.

Regionally, Asia, sometimes dominated by China, noticed a 69% decline quarter over quarter registering 108 offers for $883 million. India topped China’s funding complete for the primary time in 5 quarters. Each China and India reported 29 offers however the offers in India raised $421 million. In China, Fintechs raised simply $175 million.

Regionally, Asia, sometimes dominated by China, noticed a 69% decline quarter over quarter registering 108 offers for $883 million. India topped China’s funding complete for the primary time in 5 quarters. Each China and India reported 29 offers however the offers in India raised $421 million. In China, Fintechs raised simply $175 million.

In Europe, 108 Fintech offers generated $1.6 billion in VC funding. Evaluating to the identical quarter in 2019, Fintech funding was down solely barely whereas the variety of offers dropped from 119 in 2019.

Within the US, $3.Three billion was raised for 148 offers – down each yr over yr and sequentially. US Fintech offers dropped 23% quarter over quarter to a 13-quarter low, as funding hit its lowest level since Q3 of 2018.

So who wins the funding crown? Digital financial institution Revolut that presciently raised $500 million, at a $5.5 billion valuation, in February simply because the pandemic emerged. Timing counts.

Following Revolut within the Fintech funding line up:

So has the Fintech get together stopped? Is the funding rave over? Not so quick.

The COVID-19 was a curve-ball that nobody may hit. However on the similar time, conventional monetary companies are actually transferring sooner to replace their tech stack, go digital and innovate at a extra fast tempo. The report states that curiosity in digital innovation stays excessive. Operational effectivity counts.

The portfolio mixture of rising Fintechs might change however innovation in monetary companies is a part of a decades-long megatrend. The Coronavirus has compelled a short lived pause and compelled Fintechs to refocus.

There was a number of chatter concerning the destiny of Fintech lenders up to now few weeks. The COVID-19 pandemic has hammered on-line lenders as sources of capital have shied away and a few debtors have backed off. Current debtors usually are not all the time making funds on loans. LendingClub (NYSE:LC) lately reported that it anticipated a 90% drop in mortgage originations this quarter. Right now, Fitch Rankings stated that the impression of COVID-19 might imperil the viability of some market originators.

In a separate write up on Forbes right now, it was reported that OnDeck (NYSE: ONDK) is on the market having employed Evercore to pitch the platform. The attainable switch was described as a “fireplace sale.”

In 2014, OnDeck IPOed at $10 a share with the inventory worth rapidly leaping to over $20/share. Right now, OnDeck trades for lower than a greenback thus representing a critical decline in worth. Its market cap stands at underneath $50 million.

Late final month, OnDeck reported a quarterly lack of $0.92 per share. The consensus estimate, in response to Zacks, was $0.06 – thus representing an enormous miss.

Through the earnings name, OnDeck stated it was pushing pause on new time period mortgage and line of credit score originations. The web lender stated it can concentrate on serving current clients and supporting the PPP program, in the interim. The corporate has additionally taken “aggressive measures” to scale back prices together with an throughout the board 15% wage discount and a 30% reduce for the OnDeck CEO and board compensation.

CEO Noah Breslow said throughout the name:

“… this difficult and dynamic working setting clearly has a really direct impression on the small enterprise lending panorama wherein we function, creating close to time period headwinds, in addition to long-term alternatives together with potential consolidation inside our business. We proceed to work with our board to discover all choices to maximise shareholder worth.”

India-based digital financial institution RazorPay introduced on Could 11, 2020 that it’s planning to recruit extra employees members for key positions throughout its engineering and product design groups.

As beforehand reported, the banking challenger had revealed that there had been a big enhance within the variety of digital transactions within the nation, following the COVID-19 outbreak.

There has additionally been a rise within the variety of corporations or companies which can be both contemplating or have already adopted digital funds strategies as an alternative of dealing in money.

Razorpay confirmed that it has employed professionals for greater than 50 key roles throughout its backend, frontend, information sciences and product administration departments. The brand new hires can be tasked with coping with the elevated demand for the corporate’s companies in the course of the pandemic.

The Coronavirus disaster has been a turning level for India’s Fintech business. Though the pandemic has led to financial uncertainty and positioned important monetary stress on many companies, there are additionally many new alternatives which were created. As an example, there’s been an increase in demand for digital funds and on-line platforms typically.

Many Indian corporations are re-evaluating their enterprise fashions, revising their development and growth methods, and making obligatory adjustments to their hiring plans. Companies have additionally realized that they might wish to take into account prioritizing sustainable development and buyer acquisition over profitability throughout these difficult instances.

Anuradha Bharat, head of individuals operations at Razorpay, acknowledged:

“The way in which I see it, the Fintech sector is at its thrilling greatest proper now as everybody needs to have an e-commerce presence. Whereas there are large layoffs occurring round, we see this as a chance to rent nice minds and make high quality additions to construct a league of next-gen cost and banking options to assist with the present circumstances.”

Bharat added:

“With enterprise calls for and behaviors altering quickly throughout this time, we’re hiring for essential roles based mostly on how productive a job may be to the corporate and the business at this level. New group members include a selected model of enthusiasm and power, and as a quick evolving group, there’s a fixed need for relentless enthusiasm and high quality skill-set to complement these new roles and features.”

Throughout the previous yr, Razorpay has elevated its headcount from 330 to 770.

The corporate claims that there’s been an elevated demand for digital funds, notably because the previous six months. The agency’s neobanking division, RazorpayX, has been aiding corporations with higher managing their money flows and with acquiring key insights about their monetary development.

Based in 2014, RazorPay is reportedly solely the second Indian firm to be part of Silicon Valley’s largest know-how accelerator, Y Combinator.

Six months in the past, nobody may have predicted the place we’d be at the moment. Whereas the panorama for inventive individuals is altering earlier than our eyes, we’re working laborious to maintain evolving and bettering Patreon. That approach, regardless of the place the world leads us, you possibly can higher interact together with your neighborhood and proceed to develop your inventive enterprise.

Right here’s a recap of what we’ve been as much as over the previous six months, and in addition, what’s approaching the horizon for Patreon.

Final September, we set out on a mission that can assist you get and maintain extra patrons. We started by zeroing in on the fan to patron expertise, so we may higher perceive what we may construct to have the most important affect on the expansion of your membership.

That analysis led us to an necessary perception: because it seems, followers testing your Patreon web page for the primary time have completely different wants and questions than present patrons do. This led us to our subsequent query — if followers and patrons have completely different wants, why have they got practically an identical experiences once they go to your creator web page?

So, we created a separate touchdown web page for followers who aren’t but patrons that has an excellent clear show of tiers and advantages. Then, we ran a collection of assessments to see which model carried out finest, and rolled out the profitable model to all creators. With the modifications we made to your touchdown web page, on common 20% extra followers are selecting to grow to be patrons, which implies much less work so that you can convert your followers into patrons. Since making these modifications, we’ve continued to watch common pledge dimension and have discovered no lower within the pledge quantity creators are receiving from patrons.

Whereas that interval of speedy change to your touchdown web page is cooling down, Patreon is without end looking out for tactics that can assist you flip extra followers into patrons. Early assessments present this new design with an inventory of profit icons would result in much more followers turning into patrons. Right here’s an early tackle how that would look:

Our analysis and knowledge inform us {that a} patron’s first moments of membership are crucial to retaining them round for the lengthy haul. That second of clicking “pledge” must be as impactful as potential, immediately whisking your new patrons into all of the laborious work you’ve put into making your membership really feel particular.

So we created a model new welcome expertise and house for all issues advantages, giving followers a simple entry into the world they only uncovered by turning into your patron. And, if they’ll’t discover one thing of their advantages, we additionally added a search field, so your patrons can search and filter by means of posts to search out precisely what they want.

Along with these updates, now you can curate these crucial first moments your self by pinning a submit for brand new patrons to see in your Patreon web page, or by crafting welcome notes particularly for the tier they select.

Not solely are all of those updates a a lot better expertise for brand new patrons, on common, seven days into these modifications, we noticed an eight % drop in patrons cancelling their pledges to creators.

In January, we introduced that we’re taking Patreon world. Whereas we’ve all the time been enthusiastic about our worldwide creators and patrons, we’re now making the assist of the worldwide inventive neighborhood a central a part of our mission.

Listed here are a few of our first steps towards that purpose:

The identical approach that an awesome singer can take a basic normal and put a contemporary spin on it, we would like you to have the ability to put a singular spin in your membership, so you possibly can construct memorable connections together with your largest followers and interact your neighborhood for years to come back. And it shouldn’t be a full-time job to handle.

With that in thoughts, right here’s what we’ll be engaged on over the approaching months. Consider Patreon as your backing band, offering you a rock strong basis to make one thing distinctive and memorable in your patrons.

We are able to’t wait to share extra particulars quickly on our weblog and neighborhood discussion board!

{kind=link}

{kind=link}

{kind=link}

{kind=link}