Uncategorized

UK Crowdfunding Affiliation Feedback on FCA Expensive CEO Letter Despatched to Platforms

Two weeks in the past, the UK Monetary Conduct Authority posted a “Expensive CEO” letter directed at funding crowdfunding platforms. The letter, signed by Debbie Gupta, Director of Shopper Investments Supervision, cautioned platforms on each the chance of investments being provided to buyers in addition to the necessity to mitigate total platform threat.

Gupta acknowledged within the letter:

“Our goal is to make sure crowdfunding corporations promote funding alternatives appropriately so that buyers can perceive the dangers these speculative and high- threat investments pose. This mitigates the chance of inappropriate investments and reduces the chance of sudden losses, as highlighted within the FCA’s Name for Enter on Shopper Funding, printed in September 2020. We additionally wish to be sure that, within the occasion of failure, a agency can wind down in an orderly method by having an efficient wind down plan and holding satisfactory monetary sources.”

The letter continues to precise concern that buyers are taking part in securities choices with out totally appreciating the chance and whereas platforms require buyers to acknowledge their cash is at a heightened threat, the regulator worries that buyers “merely click on by way of the method” expressing an opinion that people should not essentially able to making valued selections.

The FCA is contemplating learn how to increase its guidelines in terms of the promotion of those investments – a transfer that might clearly affect the operations of those on-line funding platforms in addition to the corporations in search of development capital on-line.

Crowdfund Insider reached out to the UK Crowdfunding Affiliation (UKCFA) for his or her perspective. A consultant shared the next assertion:

“The letter was issued to all investment-based crowdfunding platforms on July 2nd and highlighted plenty of issues regarding high-risk investments which have been raised within the FCA dialogue paper DP 21/1. The UKCFA supplied a really detailed and in-depth response to that dialogue paper together with the survey of greater than 2500 prospects of member platforms which confirmed that regulated funding crowdfunding and p2p lending platforms have been doing an excellent job total of constructing positive prospects understood the dangers of investing (and the way prospects weren’t supportive of using blanket advertising and marketing bans on particular product classes resembling property funding).

The FCA have since been in contact straight with a pattern of platforms to say that they are going to be finishing up additional information assortment and evaluation (particulars to be confirmed) to comply with up on the proof supplied by the affiliation and perceive higher the client perceptions and expertise of the regulated crowdfunding and p2p sector.”

The UKCFA shared a replica of the aforementioned survey that gives empirical information with regard to investor participation in crowdfunded securities choices. So what do folks say concerning the crowdfunding sector?

The survey, which was carried out in June of 2021, signifies that prospects have an excellent understanding of the dangers and advantages of investing through funding crowdfunding platforms together with peer-to-peer lending websites. Simply 0.7% of respondents indicated that P2P/crowdfunding represented a low-risk funding – in different phrases, buyers know these might be dangerous investments.

Similar to different asset courses, buyers perceive that diversification is vital to threat mitigation – each throughout totally different investments in addition to totally different platforms.

Prospects are mentioned to be “strongly opposed” to “mass advertising and marketing bans” by regulators for most of these investments.

So in short, the overwhelming majority of people taking part in funding crowdfunding perceive these might be dangerous ventures, considerably in distinction to what the regulators look like claiming.

The survey states:

“We don’t imagine that generalised conclusions ought to subsequently be utilized when attempting to grasp the client outcomes of particular funding merchandise. The UKCFA would sturdy argue that the programs and controls which regulate the sector have confirmed remarkably efficient and whereas there are all the time enhancements primarily based on the findings of the analysis (notably buyer responses concerning the significance of threat warnings in supporting knowledgeable selection) the perceptions of the sector relative to different monetary merchandise would appear to be each correct and applicable.”

The UKCFA mentioned the survey outcomes got here from over 2500 prospects of member platforms providing fairness, debt safety, and loan-based investments.

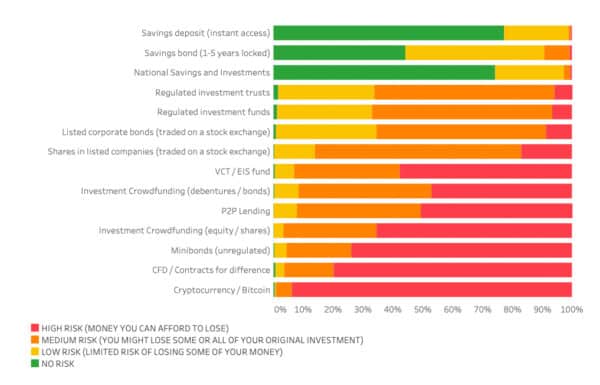

Importantly, UKCFA reaffirms that it has all the time been “pro-regulation” recognizing {that a} well-regulated trade builds belief amongst customers whereas pointing to the necessity to allow monetary innovation as crowdfunding platforms have launched a brand new asset class for a lot of buyers. Prospects of on-line funding platforms additionally usually tend to maintain numerous investments. The beneath graph helps to spotlight threat notion from the surveyed viewers with fairness buyers noting these are high-risk investments or “cash you possibly can afford to lose.”

Whereas the info seems to strongly assist the funding crowdfunding trade and pushes towards aggressive regulation by the FCA, anecdotal studies can create a notion which will differ from actuality.

A latest case the place a Crowdcube investor was awarded compensation by the Monetary Ombudsman Service (FOS) for an funding in a agency that failed may very well be misconstrued because the rule and never the exception. The letter by the FCA that nervous that “too many customers are nonetheless investing in inappropriate high-risk investments which don’t meet their wants” might foreshadow extra restrictions for the crowdfunding sector – restrictions that will not be needed.

Innovation is all the time laborious – much more so in a extremely regulated trade like funding crowdfunding (in addition to Fintech usually). And politics can cloud balanced judgment when in style sentiment drives the narrative. The UK Monetary Conduct Authority has lengthy been lauded for its forward-thinking method in empowering monetary innovation – a key variable within the UK rising as the highest world Fintech hub. The stability between market threat and regulation will all the time be a tightrope act however the price of too restrictive guidelines may very well be far higher than the combination funding loss in a sector that have to be measured by the few successes that emerge over years.