Uncategorized

Secondary Market – Jan/Feb 2021 replace

What a begin to the yr for Seedrs Secondary Market with January and February openings coming near document months at £796ok and £1.13m transacted respectively. The earlier excessive was again in Might ’20 at £1.28m so these two opening months are a fantastic begin for 2021 and simply quietly, the market tipped over a complete of £10m of secondary trades throughout 30ok share tons – fairly a mark contemplating virtually 20% of has come within the final 2 months!

In February’s market there have been 656 consumers, 718 sellers who between them bought 215 companies throughout 1,810 share tons with about 80% of the worth coming from share tons larger than £1k. The final two markets have been pushed by a handful of very massive (particular person) consumers. In February the highest three consumers by worth accounted for 30% of all transactions as they clearly noticed worth to be captured. So the ‘huge’ cash on this time of nice uncertainty is discovering solace in alternatives discovered firstly in personal secondary markets and secondly in our personal secondary market!

Sellers conversely banked and common revenue (after charges) of £1k every, not a nasty contemplating the common bought per vendor was £1.5k!

The sharelot gross sales quantity by value tier in February had been as follows:

These sharelots will be damaged out by sector as follows:

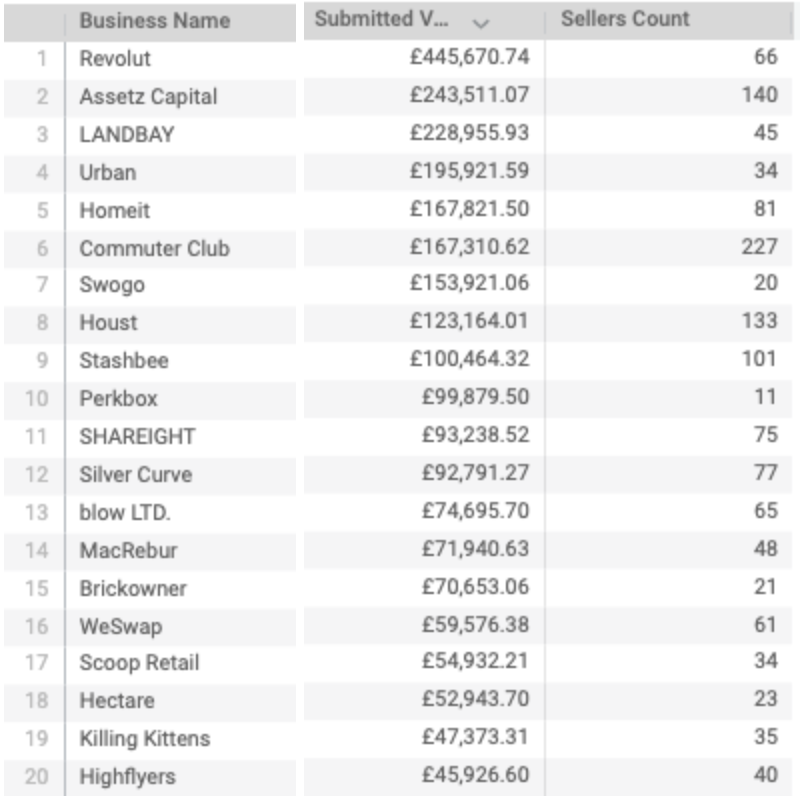

High 15 whole worth transactions by enterprise as follows:

I’ve additionally discovered it very encouraging that during the last 6 months we now have seen extra sellers and the worth per vendor rising. That is precisely as we might have hoped and anticipated with the introduction of variable pricing…

Over the identical time interval we now have additionally seen the variety of companies enhance steadily together with the worth per enterprise.

So while you possibly can clearly see a lot of the worth is being pushed by a small variety of consumers and companies, the elevated exercise is having a ripple impact.

From month to month some extent of consternation from consumers (significantly of the type after companies) is when sellers don’t affirm the sale. We frequently get requested why this step is important and why we don’t repair it. We’ve gone into element about why right here and within the gentle of our variable pricing enhancements we can be revisiting this recommendation once more. Within the meantime I believed I’d share some details on this behaviour, in February we misplaced £14.7k in unconfirmed share tons, 24 tons had been cancelled by the vendor and 43 weren’t confirmed. This represents about 2% of the worth / quantity of tons bought and is a few proportion factors beneath common so maybe with elevated warnings and the deterrents of not confirming a sale launched, this has had an affect.

The February market additionally noticed the ultimate implementation of a variety of further limitations we placed on pricing and fractional shares submitted in a share lot. We discovered with all limits eliminated a small variety of sellers had been itemizing numerous small fractional shares at very massive mark-ups thus creating a fairly small share lot measurement however containing shares with a very distorted value markups. As of February, share tons are restricted to entire shares solely (besides the place they symbolize 100% of your holding or the place the share value is larger than £100) and to a most mark-up of 500% thus considerably eliminating this behaviour.

Subsequent market is shaping up as typical, sturdy provide throughout the board with £4.8m in worth already submitted on the market, a close to document variety of companies at 451 (earlier 458) and a pair of.5k sellers (earlier 3k which was document). High companies listed on the market are as follows:

Observe: not all companies can be eligible for itemizing, eligibility checks are carried out the day earlier than market opening.

Right here’s to a different profitable March market!

Joel Ippoliti

Chief Product Officer